How could computable contracts improve people’s health insurance contracting?

by Nora al-Haider, Luz Daniel, Shobha Dasari, Margaret Hagan, Arianne Marcellin-Little, Alistair Murray, Michael Perlmutter, Roland Vogl, and Annie Zhu

This piece was originally published at our Legal Design & Innovation medium publication.

- Key Opportunities for Human-Centered Computable Contracts

- The Class’s Basics

- User Research to understand people’s journeys through health insurance

- Pain Points

- Personas of health insurance users

- People’s Stories & Quotes about health insurance

- Agenda for Change Based on Users’ Experiences

- Can Computable Contracts help?

- Prototypes for computable contracts in health insurance

- What Next? Takeaways from Our Prototype Testing

- Computable Contracts and the Law

- Future Work

In Winter 2022, our team at the Legal Design Lab worked with our Stanford Law Colleagues at CodeX to teach the class “Human-Centered Computable Contracts”.

This is part of ongoing work at both the Legal Design Lab and CodeX. Our Lab has been working on improving contracts, terms of service, and other legal text that people must grapple with to protect themselves. We’ve taught classes at the law school and d.school on these topics & have documentation of what we’ve been learning.

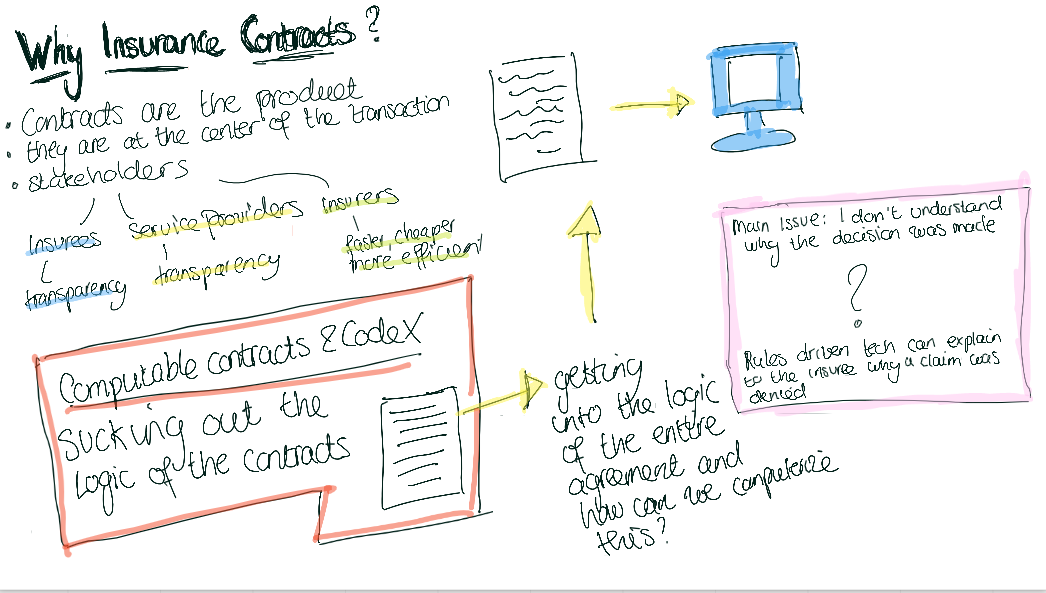

CodeX has made computable contracts a central theme for the coming years. Their Insurance Initiative is pioneering new ways to make contracts machine-readable, create a standard language for contracts, and pilot new ways to improve contracts in insurance use cases.

Our goal with the course — and ongoing design work with computable contracts — is to make sure that as this new technology develops, it’s done with real people’s concerns, frustrations, capacity, and dignity at the center.

Of all the ways we can improve the infrastructure of contracts and how they are deployed, what will people be able to use — and to get them better insurance and health care?

Key Opportunities for Human-Centered Computable Contracts

Before diving into the details of the class, our user interviews, and our initial brainstorms, it’s worth jumping to some of the big takeaways. What should people working on improving contract experiences be focused on, to truly solve people’s fundamental problems?

“Let Me Know What You Know”: Tools to Address Information Asymmetry

The most central problem in the consumer-insurance provider-health provider relationship is information asymmetry. Even if you are a power-user, who is doing everything you can to figure out how to be wise when it comes to saving money and getting the necessary care — you still cannot find out what things actually cost until after the event has happened, choices about care have been taken, and claims have been filed.

People, especially more proactive users, want tools that start to balance out this knowledge. They want tools to help them

- know before purchasing a policy how it will play out in key situations they expect might happen (a back surgery, an urgent care visit, a pregnancy, disability support, etc…)

- know what different claim codes will be covered or not, before they actually go for service from a certain medical provider and with certain claims being raised

This could be in the form of chatbots, price predictors, shopping quizzes, or even more intelligent phone calls with customer service. But they want to know what the customer service reps at the insurance companies and health care providers know. What are the real prices of things? What are the possible ways a messy life problem might be encoded into claim numbers? And what are the strategic decisions a person can make before they get encoded into a certain claim path & have to deal with the bills that might follow?

Computable contracts, paired with open data sources from health providers or insurance companies, can be a foundation for these tools to address information asymmetries.

“Give Me Something I Can Rely On”: Tools that Give Ground Truth & With Assurances

Information tools are not enough. Many consumers have been burned by previous interactions with insurance or health providers, where they have been given information by a customer service rep or policy — and then found out later that it was not reliable. A bill ended up being way more. A procedure wasn’t actually covered. The provider wasn’t actually in the covered network.

More proactive consumers try to get to a ‘ground truth’ right now by triangulating extensive research. They call the insurance company’s customer service reps multiple times, to speak to multiple people, and compare their responses to find out what they can rely on. They go to Reddit boards, Facebook groups, and chat with friends to find other people who may have ‘ground truth’ experiences that are comparable. What will actually happen to me? Who can I trust to tell me the truth?

Recent policy changes in the US may let consumers contest bills that turn out to be surprisingly high. Another direction would be for providers to have to honor the price that a person receives from a computable contract-powered tool.

A person, before they use a service or buy a policy, can use an intelligent tool to get a prediction of the out-of-pocket cost and claim coverage for a certain service. They can save this and rely upon it. If they do use this service, and the price turns out to be higher or the claim is denied, then they can show the prediction to contest the decision and protect themselves.

Computable contracts tools’ value will be in how reliable and binding they are. They need to give some guarantees to the consumer to get to the fundamental mistrust and betrayal that most consumers have toward their insurance companies.

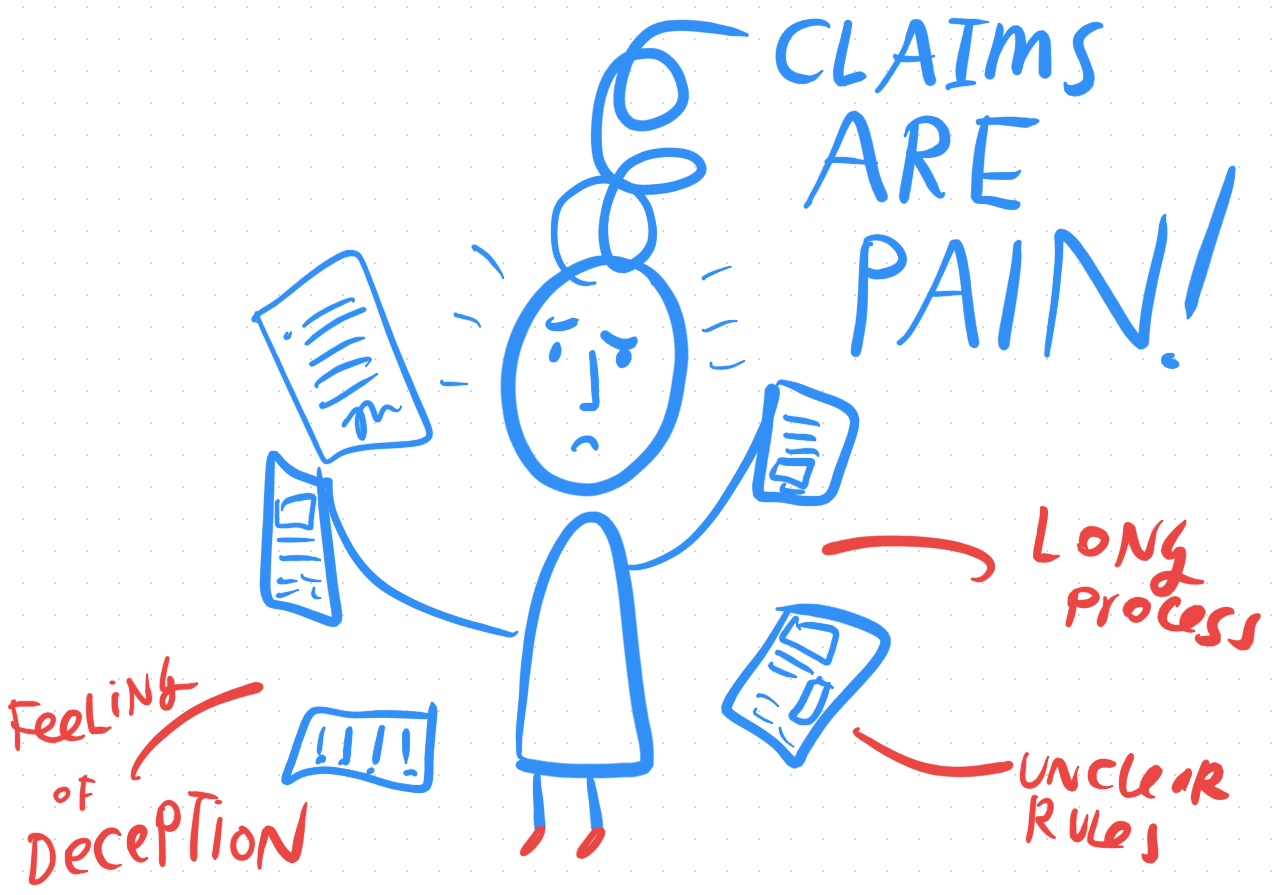

“Why Does This Have to Be So Crummy”: Design a Claims Process that is Empathetic and Supportive

When people try to make use of their insurance policies, often the process is murky, painful, and stressful. The consumer is often the last to know what is happening, as the other 2 parties — the insurance provider and health provider — are in communication making important decisions.

Plus there are opaque and overwhelming statements that come to the consumer, about possible amounts they may owe, claim codes about what services they have used, and ultimately an amount due as soon as possible, or a collections company might start hounding them.

The user does not feel like she is in control, or has a sense of dignity. There is no delight in the claims-making or -processing journey. People feel like no one is on their side — and the other 2 parties seem to be ganging up on them, to try to push their companies’ financial responsibilities onto the person with the least power and money. People want an advocate, someone on their side.

Computable contracts, mixed with new service design-oriented offerings, could help transform this process. What if there was more transparency & sense of control for the user before, during, and after the claims process? What if they felt that the price they were paying was agreeable, worthwhile, and acceptable — because they had more of a choice in deciding to make use of the service at this price, and because they have tools to contest it when it is too high.

Even more, insurance providers could think about proactively giving service maps — -with expected claims, services, and costs, to people who are on a certain medical journey. Whether a person is starting off with a pregnancy, fighting a disease, or treating a disability, the data about past claims and costs could be used to provide sample maps to consumers about what other people have done to make use of medical services in wise, financially affordable ways. The insurance provider can use its knowledge of so many consumers’ journeys to help a person plan out their use of services and risks they will take, to make sure they are doing it as wisely as possible.

The Class’s Basics

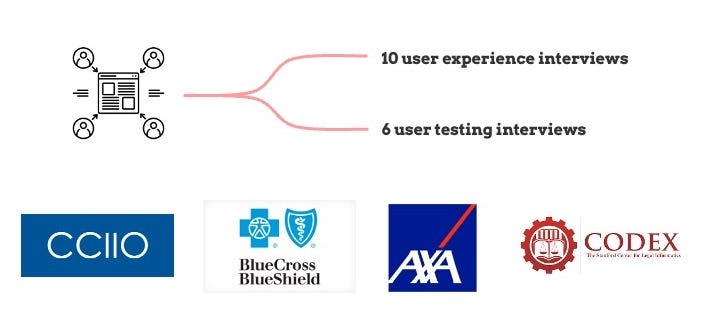

Our joint class Human-Centered Computable Contracts was taught as a policy lab, meaning we were able to do project-based work in partnership with a public interest group. In this case, our partner was the federal government group CCIIO (pronounced suh-sigh-oh), the Center for Consumer Information & Insurance Oversight. It is part of the US Centers for Medicare and Medicaid Services.

During the 9-week class, we had two main phases: exploratory interviews with people about their health care insurance contract experiences, and then prototyping and testing possible interventions (including around computable contracts) with people. Our goal was to learn more about whether and how computable contracts could benefit people in their health care and insurance activities.

We taught the students many service design techniques to make sense of the interviews and research: journey mapping, persona creation, and user story-telling. In addition, we did creative brainstorming through different structured activities. We drew from formal presentations on what computable contracts are — to then think through: how exactly could we make them useful to the people we’ve spoken with? The students made concept posters and tested the top five concepts with users to get their feedback.

We had a terrific, tight group of students who came from a mix of backgrounds. We had law students, computer scientists, and public policy students. Some had past experience as practicing lawyers, health care policy analysts, and technologists.

User Research to understand people’s journeys through health insurance

We began the class with the simple question: What are people’s experiences with health insurance contracts? And we also held on to a second question (more for the second half of our class): What are key opportunities for Computable Contracts to improve experiences & outcomes in health insurance?

We took a design approach to answer these questions. That meant talking to many stakeholders, including people who have been consumers and users of health insurance, as well as experts. During the quarter, the students and teaching team conducted 10 user experience interviews and 6 user testing interviews.

The teaching team recruited interviewees through social media advertisements and an intake screener. They signed up from around the country, and with different economic and educational backgrounds. Each interviewee had some experience with health insurance — some had been through multiple plans, others had their first insurance purchase this year. Each interviewee was interviewed over Zoom for between 20 and 40 minutes and compensated with a $40 gift certificate.

In the user experience interviews, we asked insurees to discuss their best and worst experiences with health insurance. We particularly asked users to discuss their experiences shopping for health insurance, making claims, and understanding coverage or prices. In the user testing interviews, we asked users to share their opinions regarding five different ideas about ways to help someone with their health insurance.

Insight into user experience was also shared in presentations and feedback sessions by Rogelyn McLean (Senior Advisor at the Center for Consumer Information & Insurance Oversight), Gary Cohen (former Vice President of Government Affairs at Blue Shield of California), Clara Bove (Researcher at AXA), Raphael Ancellin (Lead Product Manager at AXA), Pierre-Loic Doulcet (Computational Contract Engineer at AXA), and Michael Genesereth (Research Director of CodeX).

In addition, the team looked at past user research into people’s experiences with health care and insurance. The Enroll UX 2014 efforts, around the rollout of the Affordable Care Act, has very useful documentation of their user research into health care insurance customers.

What We Found in User Interviews

From our interviews, we learned that one size does not fit all when it comes to user needs and preferences.

Insurees’ needs and behaviors are influenced by their level of health insurance literacy and proactivity in seeking to fully understand their plan. However, regardless of specific needs or circumstances, all users want to save time and money in the processes of choosing, understanding, and using a health insurance plan.

Currently, information asymmetry between insurance companies and insurees is a source of time and cost inefficiency for the latter, who may be hindered in choosing the best plan or medical care to meet their needs if relevant information about insurance plans is inaccessible (or accessible only through a time-consuming search) or difficult to compare.

In addition, more information does not lead to more empowerment. Often the information available is obscure or unreliable. People feel like they can’t get a consistent, straight answer from their health or insurance providers about what will be covered and how much they will have to pay. There is also choice overload, with the process asking a consumer to make too many complex choices to be strategic. At some point, many consumers just give in and accept what is being told to them by the more powerful other two groups (the insurance and the health providers). They feel like they cannot navigate the process to protect themselves.

Many insurees do not trust insurance companies to provide full and accurate information or to act in the insurees’ best interests. Information asymmetry is a driving factor in this mistrust. While health insurance literacy is, for some users, a barrier to choosing and getting the most of out of a health insurance plan, even for very literate users, understanding their plan is challenging when information is unavailable, difficult to locate, or out-of-date. For instance, consumers desire more information about in-network healthcare providers, particularly regarding the cost and quality of care.

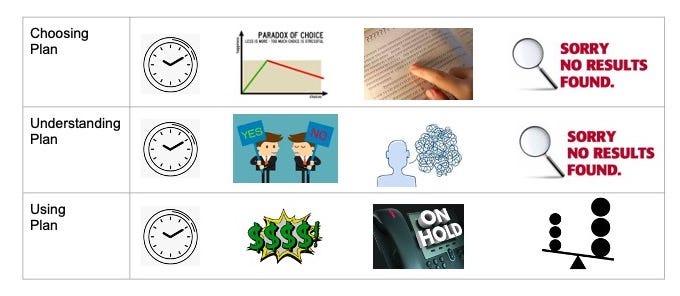

Pain Points

Choosing a Plan stage

The key pain points at this stage are time inefficiency, choice overload, health insurance illiteracy, and difficulty accessing or finding information. According to our user experience interviews, insuree frustration and time inefficiency may result from unfamiliarity with health insurance terminology, as well as difficulty finding and comparing information about different plans’ costs, coverage, and healthcare provider network.

Understanding a Plan stage

The key pain points at this stage are time inefficiency, receiving conflicting answers or vague responses from insurance company representatives, and difficulty accessing or finding information. For example, one user noted, “It’s really frustrating when you talk to different reps and get different answers. I call twice with any question to make sure their answers are the same. If they’re not, I call a third time. It’s crazy to me that someone like me who works within the system still has trouble with it. Insurance is too businesslike and not really trying to help patients. We need advocates within the system!”

Using a Plan stage

The key pain points at this stage are time inefficiency, surprise costs, inaccessible or unresponsive insurance representatives, and information asymmetry (especially regarding costs and the healthcare provider network). Having to choose whether, where, or how to receive treatment without cost information is an oft-cited insuree pain point. Ascertaining the role of referrals in insurance coverage can also cause uncertainty and stress.

Personas of health insurance users

In our user interviews, we learned from proactive and reactive users about their experiences at the stages of choosing a health insurance plan and filing claims.

At the shopping stage, proactive users may be focused on developing their literacy and fully understanding the plans that they are considering. This can be a time-consuming process, especially due to an overwhelming amount of information or plan options. Proactive users are often shopping based on specific needs, such as geographic scope or coverage of particular health conditions.

Reactive users, on the other hand, may have broader comparison concerns, such as finding the cheapest plan or the broadest healthcare provider network. Reactive users may primarily view insurance as a source of “peace of mind.” They therefore may be less motivated to examine all the details of their plan, and may rely on overall ratings or colleagues’ impressions in their decision. For instance, one user who had not yet needed to use his new insurance plan stated, “I will understand it better when I have a real situation.”

At the claims stage, proactive users seek to understand their plan before taking action. They find it difficult and time-consuming to get information about coverage and cost of care from either their insurance company or healthcare provider. Proactive users may even forgo care if costs are uncertain. Some do not trust their insurance company to provide full and accurate information, so proactive users often turn to online sources such as Reddit or Facebook to ask questions, whether due to greater trust or convenience.

For reactive users, especially if they have waited until a medical emergency to look into the specifics of their coverage, the cost of care may come as an unpleasant surprise. However, it is important to note that information asymmetry makes the cost of care obscure for both reactive and proactive users.

People’s Stories & Quotes about health insurance

Whether a proactive or reactive user, nearly every consumer we spoke with sought advice or help from somewhere other than their insurance policy contract or insurance representative when approaching a pain point.

What will it cost me to take my kid to the ER?

One consumer, who described herself as “relatively well-informed,” found the resources provided by her insurer either unhelpful or incomprehensible. When deciding whether to visit urgent care or the ER when her child became sick, she first combed through the “fine print and terms and conditions” of her insurance contract.

When this exercise proved fruitless, she called her insurer and spoke directly to a representative. Unfortunately, she didn’t feel like her questions were answered and she was no clearer on whether it would be more affordable to visit urgent care rather than the ER. Before resorting to guessing, she visited a neighborhood mom’s Facebook group where she posed the question to the community and asked for their advice. She gained valuable information that was immediately intelligible and that she trusted. Whether the information she received was correct is hard to say, but it allowed her to feel confident in making a decision — something she didn’t feel after combing her contract for information or speaking with her insurance representative.

What should I do about my back?

Another consumer we spoke with found herself in a somewhat similar situation but wound up with a different result. After physical therapy failed to cure her back pain, she decided to undergo surgery, which her doctor assured her would resolve her injury. Her doctor promised to send a pre-authorization form to her insurer. One week before her scheduled surgery, she discovered the doctor’s office had failed to submit the pre-authorization paperwork.

When they finally did, however, the insurance agency told her it was impossible for them to approve the surgery so quickly. She argued for an expedited turnaround, which the insurer agreed to. But, on her way to the surgery, they told her they still hadn’t made a decision. She decided to forgo the surgery and continue enduring the physical pain instead of going through with the surgery without knowing how much of its cost she would be required to cover.

Here, the lack of transparency and the slow process of a seemingly discretionary authorization prevented a patient from seeking medical care she could have used. No Facebook group could have answered this question for her and given her enough confidence that the surgery would be covered to feel comfortable undergoing the surgery.

Who can tell me the real information about this insurance?

A third consumer spoke about different avenues of information gathering he sought beyond his insurer. Whether shopping for insurance or, like the two consumers described above, making decisions about medical care, he found it useful to peruse Google, Facebook, and Reddit and to speak with friends and colleagues. Like the other consumers we spoke with, he found insurers the least informative and most difficult to get a comprehensible answer from. A different consumer told us that she calls her insurer twice whenever she has a question to make sure the first answer she received was correct. If she receives two different answers, she’ll call a third time.

Many of the stories we heard were disheartening and frustrating. The stories described above are only a small sample, but they are representative of the sort of stories we heard during our interviews. In the end, everyone is operating under their own unique circumstances. It boggles the mind that consumers should feel they’ll get better information from a stranger on the internet who knows nothing about the idiosyncrasies of their needs or the contract they have with their insurer than they would by simply calling their insurance representative or reading through their contract of SBC. But, as it is, consumers are operating under a severe information asymmetry with respect to their insurers.

This information asymmetry is not resolved by insurance representatives, insurance contracts, or SBCs. As such, it causes consumers to look elsewhere for help. But the help they receive may not lead them to the best answer. Consumers are inefficiently spending their time gathering information and making cost-inefficient decisions about their healthcare that may have detrimental effects on their own health. Nearly every consumer we spoke with expressed despondency at the fact that nobody was advocating for them from within the system, that they were constantly on their own and information was constantly out of reach.

Agenda for Change Based on Users’ Experiences

The success of insurance marketplaces is related in part to consumers’ ability to understand health insurance contracts and make informed decisions[1]. Competition at the consumer level is likely to reduce prices and improve quality when a sufficient number of consumers make informed decisions[2]. However, consumers can also make suboptimal decisions when faced with overly complex choices[3] or too many alternatives[4].

Moreover, the information asymmetry permeating the health sector represents an obstacle to regulating and promoting competition within this market. In this sense, insurance purchasers who cannot understand health plan offers will find it difficult to make rational decisions regarding the insurance company they wish to contract.

Regarding the problems detected in the private health insurance market, the government has made progress in reforms to reduce information asymmetry and empower consumers to make better decisions. Among these reforms, we can highlight the following:

Hospital Price Transparency

This regulation requires the hospitals operating in the US to provide clear, accessible pricing information online about the items and services they offer. This information but be machine-readable with all items and services and must be displayed in a consumer-friendly format. The main objective is to make it easier for consumers to shop and compare prices across hospitals and estimate the cost of care before going to the hospital.

The government’s major reform efforts have contributed to improving this market. However, future efforts should aim to resolve the pain points consumers face[5].

Summary of Benefits & Coverage

This reform aims to present the consumer a snapshot of the health plan’s costs, benefits, covered health care services, and other essential features. The main objective of this regulation is to help consumers –in the shopping phase — to compare different elements of health benefits and coverage[6].

Metal plans

The Affordable Care Act standardized small-group and individual health insurance policies by creating a “metal” ranking. All the health plans are categorized into Bronze, Silver, Gold, and Platinum metal tiers. Each category offers different ratios of what you will pay and what your health plan will pay for your care.

The government’s significant reform efforts have contributed to improving this market. However, future efforts should aim to resolve the pain points consumers face, such as time inefficiency, choice overload, and lack of health insurance literacy. We believe that technology and computable contracts can be great tools to resolve these pain points we saw in the interviews. The adoption of computable contracting by the insurance companies will create improvements in efficiency for these firms and benefits for consumers[7].

Can Computable Contracts help?

In the second half of our course, we moved from general empathy and exploratory interviews with consumers — to diving into possible solutions.

Computable contracts, in particular, were discussed as a way to improve information transparency, speed of processing, and consumers’ ability to make strategic choices. The students heard from experts at CodeX who are establishing standards and pilots of computable contracts to hear how they might work in the health insurance space. Then they had to develop proposals about human-centered computable contracts to improve people’s health insurance experiences.

In insurance, the product is the contract, different from many other industries. From a consumer perspective, these contracts are often difficult to understand and this information asymmetry between insurers and insurees produces mistrust from customers in insurance companies.

In our research, we identified 4 main consumer pain points with regards to health insurance, which was the focus of our research:

- time inefficiency,

- choice overload,

- information overload, and

- lack of health insurance literacy.

What’s a computable contract exactly?

The automation of contracts through computable contracts presents a positive opportunity for both insurance companies and consumers. According to Stanford CodeX, “a computable contract expresses the rights, duties, and processes defined in a contract directly in machine-executable code for querying, analyzing, verifying, and automating contractual obligations.”

Legal rules have a well-defined logical structure that makes them feasible to define in a program. In a simple computable contract, we can program the definitions of events specified in the contract using a set of if-else rules that specify different circumstances, along with the consequences when those events occur.

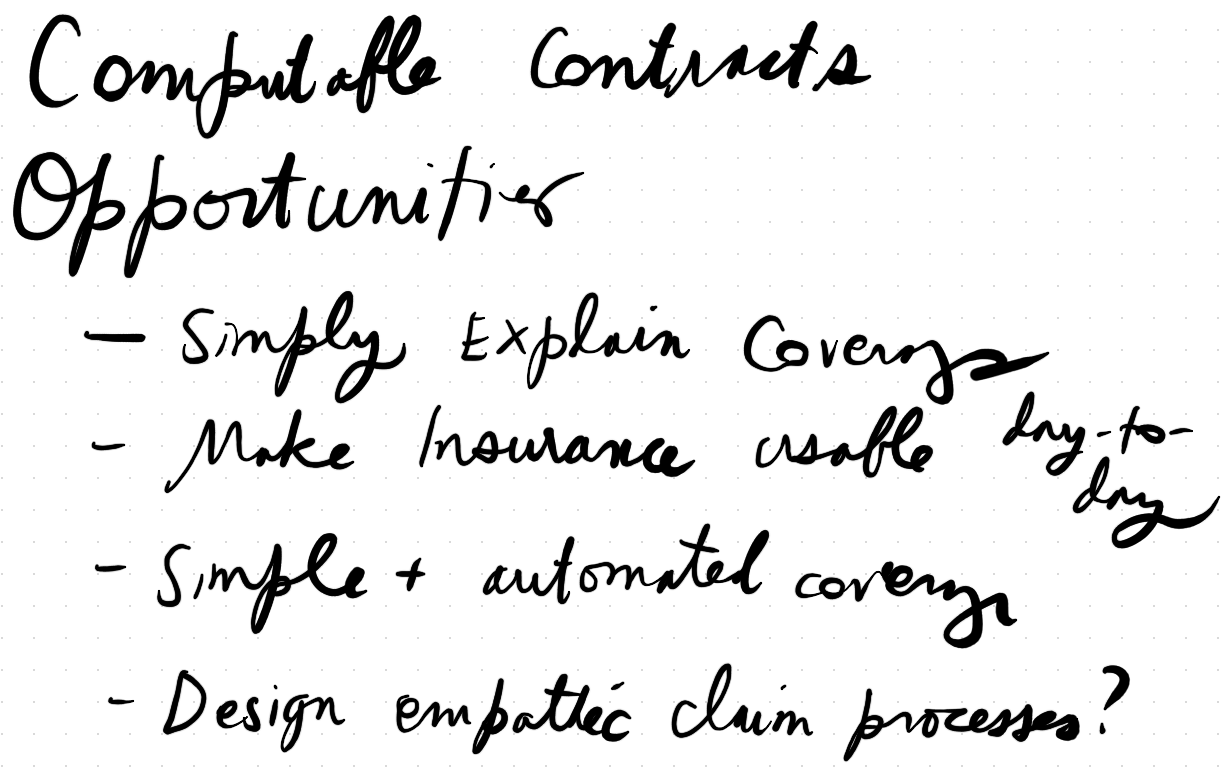

By putting the understanding of a contract into code, we unlock many new value propositions in using computable contracts. From a consumer perspective, there is improved transparency and understandability of the contract. Through a query of the computable contract, a consumer can understand how their contract applies in different scenarios, such as getting the cost of a procedure that they need to be covered by their insurance company. The computable contract may also have FAQ functions or information visualization that will make it easier for a consumer to understand the terms of their insurance contract. Insurance representatives that interact with the contract, such as sales agents or customer service will also have an easier time answering consumer questions as a result.

Computable contracts also offer the ability for insurance companies and consumers to increase the customization of their contract and policy with the company. For example, the computable contract can be modular, meaning that a consumer can take elements from different policies that fit their needs the most effectively, and create a customized policy as a result, with little change to the typical operations of the insurance company.

Insurance companies also benefit from computable contracts due to increased efficiency in their operations. Claims processing under computable contracts might only involve a few queries to the computable contract, which will make this faster and lower cost for the company. Insurance companies may also benefit from simplified underwriting due to the automation and improved precision of actuarial calculations. Regulators also benefit from the use of computable contracts, since the more structured nature of computable contracts will support internal oversight and external regulation of insurance companies.

Additionally, computable contracts can unlock new opportunities for innovation in the insurance industry. Through more structured insurance data collection and analysis, insurance companies are able to create more opportunities for the improved effectiveness of data analysis and artificial intelligence tools and research. Insurance companies will also be able to use more thorough analytics about consumer preferences and improved actuarial models to improve their policy design and pricing. Increased interoperability between computable contracts can also help improve reinsurance transactions as well as improve quantifications of risks in pooling and shared risk schemes.

Prototypes for computable contracts in health insurance

This section details our prototypes of insurance products that utilize computable contract technology introduced in the previous section and the responses we received from user testing on these prototypes. These findings are used to inform general takeaways for insurance companies and government agencies for potential next steps.

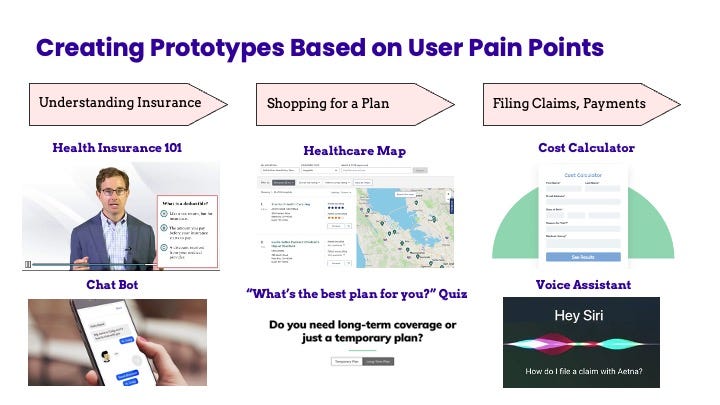

Based on our understanding of consumer pain points with insurance, our research group created five ideas for prototypes to test, grouped together based on the stages of the user journey: 1) understanding insurance, 2) shopping for a plan, and 3) using the plan.

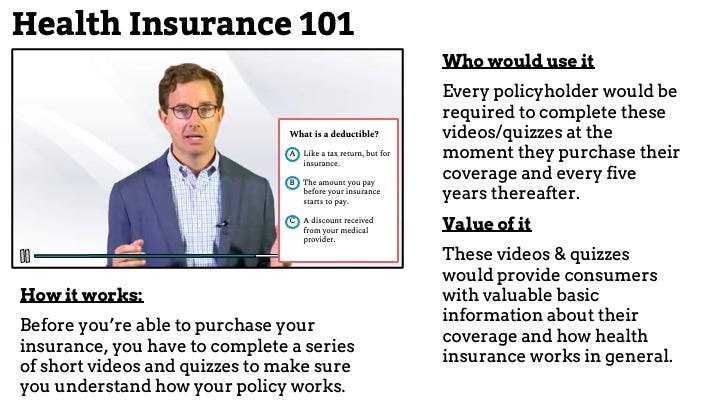

Prototype: Health Insurance 101

First, for the “Understanding Insurance” stage, we developed a prototype of an educational online training sequence which we call Health Insurance 101. The purpose of this feature is to address the lack of insurance literacy, one of the major pain points for consumers today. Consumers would be able to use this application to complete a series of short videos and quizzes to learn the details of the insurance policy.

Companies could tailor the program to educate the user about specific policies and they could require every policyholder to complete these videos and quizzes at the moment they purchase their coverage and every five years thereafter. Not only would these educational programs provide consumers with valuable basic information about their coverage and how health insurance works more broadly, but it also creates a base level of trust as transparency about policy is given from the start.

Computable contract technology would be valuable in the process of developing these programs as the first step of creating a computable contract is to identify and define domain ontologies, which can be translated into key learning points in Health Insurance 101.

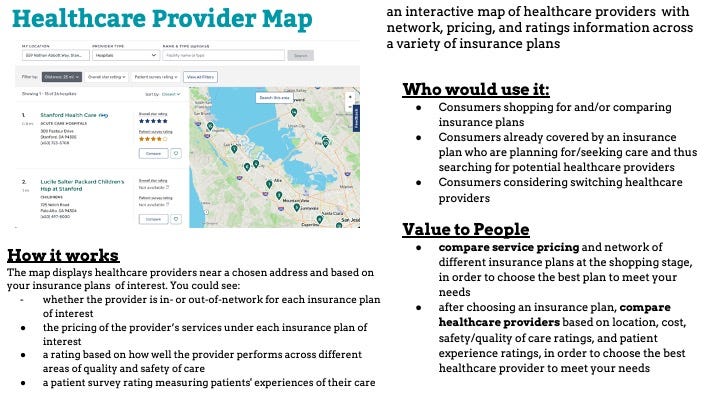

Prototype: Healthcare Map

Next, for the “Shopping for a Plan” stage, we created a prototype of a Healthcare Map that allows people to view healthcare providers near a chosen address and based on insurance plans of interest. Specifically, this application would allow users to discover whether the provider is in- or out-of-network for each insurance plan of interest, the pricing of the provider’s services, and a rating based on quality and safety of care.

Prototype: Best Plan For You quiz

Another prototype we sketched out was a “What’s the best plan for you?” Quiz. After consumers input their demographic information, health information, and insurance needs/wants, this quiz returns a list of insurance plans that fits their needs. Both of these prototypes would simplify the shopping process by resolving the choice overload issue and enabling effortless comparison between plans.

The derivation trees that computable contract technology generates would be an essential part of developing the “What’s the best plan for you?” Quiz, and would make it easy to program the site to give an explanation of why certain plans are recommended. This technology could also be leveraged to create filters for the searching capability on the Healthcare Map since computable contract technology helps organize terms in a machine-readable script.

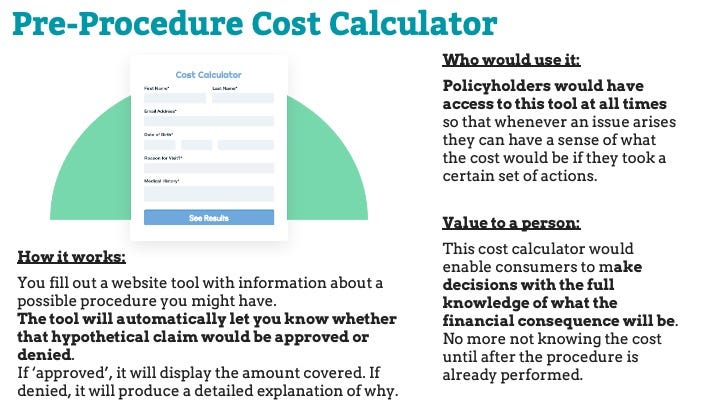

Prototypes: Cost Calculator & Chatbot

Finally, for the “Using a Plan” stage, we prototyped a Pre-Procedure Cost Calculator and a Logic-Programming based Chatbot.

For the Cost Calculator, consumers are able to fill out a page with information about a possible procedure, and then the tool will automatically inform the user about whether that hypothetical claim would be approved or denied.

If approved, the site will display the amount covered. If denied, it will produce a detailed explanation of why. This cost calculator would empower consumers to make decisions with the full knowledge of what the financial consequence will be.

In the case that consumers have more general questions, we formed the Chatbot prototype to help.

This application could either come in the form of an online chat or a phone call with automated responses. While this technology is already in place for many companies, computable contract technology would improve the bot’s capabilities because the heart of computable contracts is logic programming, which involves breaking down the policies into a set of rules and data, then creating an interpreter that can answer various questions.

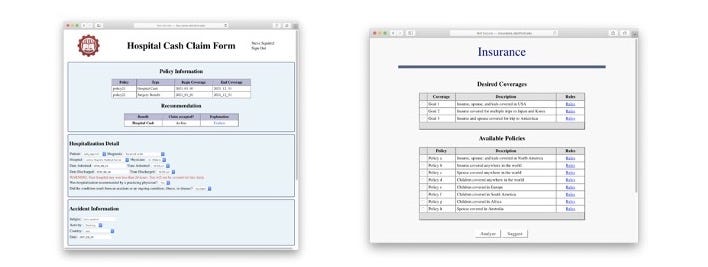

The Pre-Procedure Cost Calculator can also be programmed entirely with logic programming as demonstrated by Professor Genereseth’s research. His work with the Codex team demonstrates the feasibility of computable contracts as he was able to create a Hospital Cash Claim form based on Chubb’s hospital cash product.

Results from first round of testing

We presented these five prototypes to six people during user testing sessions and asked them to rank each product based on the prompts: “Would you use this if someone offered it to you?”, “Would this help you get a better outcome with your health insurance?”, and “How easy would this be for you to use & understand?”

These testing sessions were done by recruiting of health insurance consumers from across the US through social media ads, like with our initial empathy interviews. Users were interviewed for around 20 minutes and compensated with $40 gift certificates.

Overall, people reacted enthusiastically to our ideas and the concept of using technology to improve consumer experience with insurance. The average rating for every product is over 4 out of 5.

What Next? Takeaways from Our Prototype Testing

For insurance companies, the user testing and research into the applications of computable contracts suggest that incorporating computable contract technology into a company’s services could streamline and integrate multiple processes.

For example, improving the chatbot would significantly cut down on human resource costs needed for answering people’s questions.

Another key example could be how having a program decipher whether a claim is approved or not would decrease time spent on each claim, allowing more time and money to be spent elsewhere.

For government agencies, our work indicates that requiring insurance companies to make their policies accessible through a computable contract would increase user satisfaction and empowerment.

The feasibility of a government branch mandating companies file machine-readable reports is supported by historical precedent. In 2009, the SEC required “corporations, mutual funds, and credit-rating agencies to report information in eXtensible Business Reporting Language (XBRL), a move that simultaneously reduced the costs of compliance for firms and cut the costs of accessing information for analysts, auditors, investors, and regulators.”

The same concept can be transferred from the finance industry to the insurance industry. Computable contracts then would also make it easier for the government agencies to tell if insurance companies are complying with guidelines because the information becomes easily accessible.

Our partners at CCIO highlighted many of the upcoming changes that could feed into this better future:

- Transparency in Coverage requirements, that go into effect on July 2022. Health providers will be required to publicly post their price information, in machine-readable formats. This can be used in computable contract tools to help consumers make smarter choices.

- The No Surprises Act (NSA) that will protect people against surprise medical bills. NSA will limit how much providers can charge, and what kinds of authorization are needed to get coverage. This might be useful when combined with a pre-procedure cost calculator.

Computable Contracts and the Law

The myriad potential applications of computable contracts in the health insurance space give rise to several legal issues.

Our insurance stakeholders provided us with the example of a chatbot using computable contracts to communicate policy coverage in layman’s terms. In that case, there was concern that if policy coverage were miscommunicated or misunderstood, the insurance company would expose itself to legal liability. Moreover, computable contracts must comply with data and privacy laws, which pose a particular challenge because they are widely applicable (EU data laws could apply to American insurers if they handle data from EU citizens), varying across many jurisdictions, and rapidly developing. In the following section, we will discuss some of the most important developments and their implications for computable contracts in the health insurance space.

This section will not cover data protection statutes related to health data, such as the Health Insurance Portability and Accountability Act of 1996 (HIPAA). The California Privacy Rights Act of 2020 (CPRA) exempts protected health information (PHI) that is collected by a covered entity and medical information governed by the California Confidentiality of Medical Information Act. However, because the CPRA exempts types of data and not types of entities, peripheral data collected by health insurers are still covered by California data laws.

Developments in Data & Privacy Law

The CPRA is at the forefront of the development of data and privacy laws in the United States. The law created the California Privacy Protection Agency (CPPA) which will begin enforcing the CPRA in July 2023. Major health insurers will almost certainly need to comply with the CPRA for data not covered by medical data laws; any business with more than $25 million in annual gross revenues is covered by the CPRA. Several of the rights granted to consumers in the CPRA were simply carried over from the California Consumer Privacy Act (CCPA) and so will be familiar to insurers. These include the right to: delete personal information, know categories and specific pieces of personal information, opt-out of the sale or sharing of personal information, and non-retaliation.

There are, however, new rights granted to consumers under the CPRA. These rights include rights to correct inaccurate information, limit the use and disclosure of sensitive personal information and opt-out of automated decision-making technology. Computable contracts will need to be able to comply with each of these rights. The right to opt-out of automated decision-making technology was primarily adopted to prevent companies from using machine learning to create consumer profiles, but it could severely limit the effectiveness of computable contracts if consumers are able and choose to exercise it in the computable contract context.

It is unclear to us from a technical standpoint whether these consumer rights will be a hurdle for or benefit of computable contracts. It is possible that computable contracts will make it easier to share information about data collection, make corrections and deletions, and offer opportunities to opt-out of data collection and sharing by better-integrating health insurance information into an insurer’s technology stack. However, it could also be the case that these rights would be difficult to square with computable contracts, in which case back-end use (as opposed to consumer-facing) of computable contracts would be preferable. Back-end applications of computable contracts in contract management would still have a large impact; Bain & Company estimates that improving contract management could save up to 100 basis points (1%) of companies’ revenue. However, it remains to be seen whether this benefit would flow to consumers.

For international insurers, there’s the additional privacy concern of compliance with GDPR and European Union Court of Justice (ECJ) decisions such as Schrems II. In Schrems II, the ECJ invalidated the EU-US Privacy Shield, which had previously allowed for the transfer of personal data from the EU to the US. Though there are currently negotiations for a new iteration of the privacy shield, any similar outcome will be likely to result in another adverse ruling — that is, a Schrems III — from the ECJ because the US seems unlikely to adopt a comprehensive federal privacy bill. As such, international insurers will need to localize their European data in Europe and keep it separate from their US data. This will limit some of the risk aggregation upsides of consolidated insurance data.

Other Legal Implications of Computable Contracts

A separate item for consideration is how judges will understand and apply contract law to computable contracts. On this matter, jurist comprehensibility will be important, especially if the computable contract is closer to code in application than to a natural language embodiment. Again, however, there will likely be a “legalese” counterpart to the computable contract that could alleviate this concern. If there are few operational issues with creating, translating, and managing these counterparts, this will be a viable solution.

That said, there could be a question as to whether electronic agents can even bind their principals through the decisions they make in smart contract code. As the Chamber of Digital Commerce notes, limited contemporary precedence exists on this question. On one hand, the automatic issuance of a tracking number was deemed “an automated, ministerial act” that did not constitute contractual acceptance in Corinthian Pharmaceutical Systems, Inc. v. Lederle Laboratories, 724 F. Supp. 605, 610 (S.D. Ind. 1989). On the other hand, the Tenth Circuit affirmed a district court finding of liability for an insurance company’s computerized reinstatement of an insurance policy, stating that “[a] computer operates only in accordance with the information and directions supplied by its human programmers. If the computer does not think like a man, it is man’s fault.” State Farm Mut. Auto. Ins. Co. v. Bockhorst, 453 F.2d 533 (10th Cir. 1972).

Possible Solutions

A way forward that could meet multiple stakeholders’ interests is a standardized computable contract template — akin to the ISDA Master Agreement for derivatives — for low-complexity, high volume health insurance contracts. The ISDA Master Agreement is a standard document created by the International Swaps and Derivatives Association (ISDA) used to govern over-the-counter (OTC) derivatives (i.e., derivatives traded directly between counterparties and not traded on an exchange). The ISDA Master Agreement standardizes terms for a derivative that can then subsequently be adjusted in a customized schedule. ISDA has been exploring possible applications of computable contracts since 2017. Moreover, since its most recent revision in 2002, the ISDA Master Agreement has developed a corpus of legal decisions that reduce uncertainty over legal matters involved in OTC derivatives.

Standardization would advance CCIIO’s interests by offering consumers fewer and clearer choices that limit cognitive overload and by providing a single template for regulators and watchdog groups to audit. Moreover, it would provide consumers with a body of policy claim decisions based on a similar contract, thereby reducing consumer uncertainty over what is likely to be covered.

Standardization would also advance insurers’ interests by creating a low-risk deployment area to implement and iterate the new technology involved in computable contracts. It would also present an opportunity for jurists and regulators to decide novel legal issues with computable contracts with less financial exposure for insurers.

Future Work

Our research shows that there is significant demand from consumers to improve information access and transparency in their experiences with health insurance, and that computable contracts pose many promising opportunities to alleviate these issues.

Future work that could stem from our research includes further user testing of our prototypes, as well as other computable contract applications, in order to determine which innovations have the most demand.

Another round of user testing might include testing our prototype ideas with a larger and diverse sample size of users to see which ideas are most promising and exciting to consumers. From there, we could create low-fidelity prototypes of the ideas our groups chooses to pursue, and then test various implementations with users to see which they prefer. It would be important for us to test these prototypes with a diverse group of consumers who all have varying insurance needs to ensure that we capture a variety of perspectives in our user research.

Should computable contracts become adopted by the insurance industry, there is also a need to create educational content and materials for judges and other legal professionals to utilize them effectively. One example of this would be training on how a judge can interpret the clauses of a computable contract since this will be quite different to interpret from a contract in document form.

Overall, we believe that there is potential for computable contracts to improve access and transparency in the insurance industry. As a result, insurance companies will benefit from efficiency improvements in their operations, consumers will have an improved experience and trust in insurance, and government agencies will be able to more effectively regulate insurance companies.

[1] Paez. K. et al. “Development of the Health Insurance Literacy Measure (HILM): Conceptualizing and Measuring Consumer Ability to Choose and Use Private Health Insurance”, in Journal of Health Communication, 2014.

[2] Loewenstein, G. et al. “Consumers’ misunderstanding of health insurance”, in Journal of Health Economics, 2013.

[3] Scitovsky, T. “Ignorance as a source of oligopoly power”, in Am. Econ. Rev. 40, 1950, 48–53.

[4] See Shaller, D. “Consumers in Health Care: The Burden of Choice”, Oakland, CA: California HealthCare Foundation, 2005; Wood, S., et al. “Numeracy and Medicare Part D: The Importance of Choice and Literacy for Numbers in Optimizing Decision Making for Medicare’s Prescription Drug Program” in Psychology and Aging, 2011, 295–307.

[5] See Centers for Medicare & Medicaid Services. Available online.

[6] See Health Insurance Marketplace, Understanding the Summary of Benefits and Coverage (SBC) Fast Facts for Assisters. Available online.

[7] See CodeX, Computable Contracts and Insurance: An Introduction. Available online.